If you’ve graduated from college or graduate school in the last decade, I don’t need to tell you that college tuition is rising at an unsustainable level or that we are graduating with monstrous student loan debts—to the point that Americans’ total student loan debt has surpassed our credit card debt for the first time in history.

There’s lots of talk about the calculus of return on investment in education. I get plenty of emails from readers with six-figure student loans for degrees in social work who have a very difficult financial road ahead.

Sure, if you’re 18 and have the foresight to choose a reasonably priced college and an in-demand field of study, great. But if you’re older, wiser, and deeper in debt, how do you attack those student loans?

Specifically, if you find yourself with extra cash, should you pay down student loans early?

In most cases, I don’t think so. I recorded this video to very quickly answer why:

We’re going to get into the pros and cons of repaying student loans early versus hanging onto that money for things like an emergency fund, retirement, a home, or even just having fun. But first things first: When you’re starting down a big student loan balance, you want to be sure to do two things:

- Make a plan

- Make your payments

Make a plan

The best way to deal with your student loans is to make a plan, get organized, automate your payments and forget them. Loan consolidation can help if you’ve got lots of different lenders, but it’s not necessary if you’re organized.

I made a spreadsheet with all of my student loans, their balances, monthly payments, and interest rates. I then set up automated monthly payments through each student loan servicer’s website. (For those curious, I had student loan interest rates of 5% and 7.6% and only made regular payments until my balances were about $1,000 each—at which point I paid them off in full.)

Usually I prefer to set up automatic payments through my bank’s online billpay because I can control them all in one place. I made an exception for my student loans for two reasons:

- One of my servicers, NelNet, gave me a 0.25% interest rate reduction for having AutoPay through them.

- With loans that have a variable interest rate, the payment amount changes every so often. Having AutoPay through the servicer’s website ensured I didn’t have to remember to update the payment amount every time the rate changed.

Make your payments

Not paying your student loans is a big deal.

You probably know by now that if you stop paying a credit card bill, your credit score goes down and it will be difficult to get new credit when you need it. The bank will send your account into collections and you’ll get lots of phone calls and letters until you pay up. You can even be taken to court and a judge can order your wages garnished.

If, however, you get into such serious financial straights that you need to declare bankruptcy, a judge may rule that you do not have to pay credit card debts and you get a fresh start.

With federally guaranteed student loans, you don’t have that option. Even bankruptcy does not relieve you from paying student loans. In addition to taking you to court and garnishing your wages, the government can withhold any tax refunds. If you default on student loans guaranteed by your state’s finance authority, there may be additional consequences such as suspension of your professional license (for example, to practice law or medicine) in that state.

The bottom line is that repaying student loans is an obligation. Trying to skip the bill is a bad idea!

Fortunately, if you’re having trouble paying, there are built-in protections like reduced payment plans, grace periods, and forbearance—an extreme program in which you may be able to suspend payments for a brief period of time. In some cases, you may also be eligible for partial or complete student loan forgiveness if you work in public service.

Paying student loans early doesn’t always offer the best return

As we learn about personal finance, writers and experts drive home one point again and again: debt is bad. Avoid debt. Get out of debt as soon as possible. However, in an effort to make sure everybody “gets it,” we’ve oversimplified the equation. Not all debts are created equal.

I sometimes come across the term good debt and bad debt. “Bad” debt is bad because it either has a wicked interest rate or is designed to pay for depreciating assets like a car. “Good” debt is “good” because it’s used by appreciating or income-producing assets like a business, real estate, or an education.

I don’t like the terms good and bad because it’s hard to call any debt “good.” A debt may not be bad, but it’s never “good.” There’s bad debt, and there’s debt that’s OK to keep around because you’re using it as leverage to build more wealth than you could without it.

And that’s how I view student loans. If held to an answer, I tell most people not to repay student loans early. Instead, take that money and invest it. As long as your student loans have interest rates less than 10% over the long run, your money should do better in the stock market than the interest rate on your loans.

Look at it this way. If I gave you the choice between two investments:

- Investment A pays 10% and is liquid (you can access your money anytime)

- Investment B pays 5% and is illiquid (once you put money in, you can’t get it back for many years)

Which one would you pick?

Probably investment A. But by paying off your student loans early, you’re choosing investment B. As soon as you make a big loan payment, that cash is gone…you can’t use it for anything else: emergencies, a new home, an investment opportunity, etc. This is another reason I prefer hanging onto extra cash and investing instead of paying off a student loan early.

But…paying off student loans is a guaranteed return, isn’t it?

There is, however, one big advantage to Investment B: The return is guaranteed.

There’s no way around it: Investing in the stock market is risky. Historically, stock market returns over the long run are stable and may even be as high as an average of 8 to 10% per year. But we all know that today’s economy is uncertain. You could do better, or you could do worse.

When you repay your student loans, you get a guaranteed return. For every additional dollar you pay towards your student loan now, you save paying interest on that dollar for the remaining term of your loan. It’s as good as putting that money in your pocket. This is why, if you have private student loans with high interest rates, it makes sense to repay them early. Although you might squeeze average annual returns of 12% or more out of the stock market, you can’t count on it.

This is where the decision gets tricky: It all depends on the average annual return you expect to earn from your investments and how that compares to your student loan interest rate.

Here are three examples:

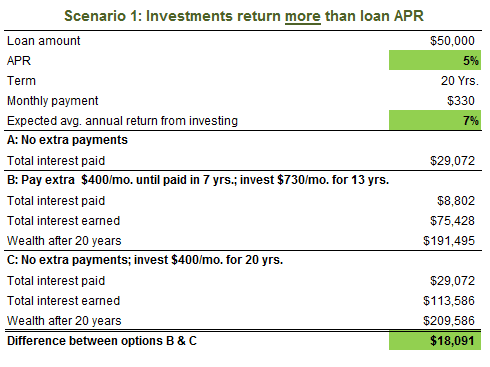

In this scenario, you have student loans at 5% and have a conservative expected annual investment return of 7%. Over 20 years, the difference between repaying your loans early and using that money to invest adds up to $18,000. So even a small difference in expected return and loan APR can add up to big money over time.

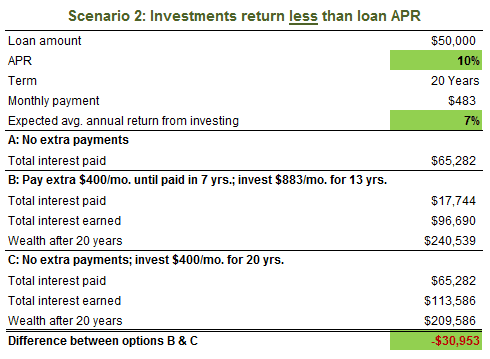

In Scenario 2, the high 10% loan APR is quite a bit higher than the 7% expected return, and investing instead of repaying the loan early means losing nearly $31,000 over 20 years. This is why it is smart to repay high-interest student loans early.

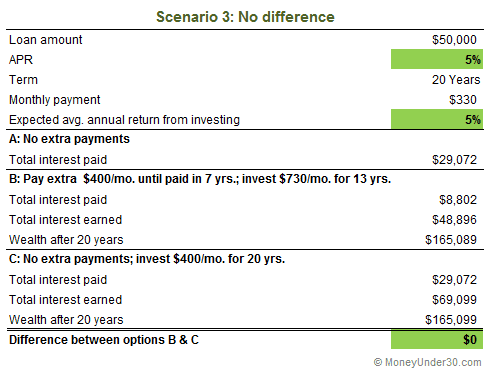

In our final example, the loan and expected annual investment return are the same. Although I personally believe you’ll do better than 5% investing in stocks over the long run, many people may disagree. In this case, whether you invest or repay the loan early, you come out even.

So what expected rate of return should you use to make your own calculation? I think 7% is a totally reasonable target and may even be on the conservative side. I’ve heard Dave Ramsey use 11 or even 12% as his expected investment returns. It’s possible, but I wouldn’t bet on it. If you’re a more aggressive investor, use 10%. If you’re more conservative, stick with 6 or even 5%.

Special circumstances

There are a few situations that change the rules.

Income-based repayment plans

Some lenders allow you to reduce your monthly payment if you don’t earn a lot. Typically this program is designed to help you get started in an entry-level job or if you’re working part-time while looking for full-time work. You’ll want to start making the full student loan payments as soon as you can afford it.

With reduced payments, you may not be paying much principal each month—or you may not be paying principal at all—just interest. At that rate, you’ll never repay the student loan—the payments will stretch on forever.

Buying a house

In some cases, big student loan debts may get in the way of qualifying for a mortgage.

Lenders require your overall debt-to-income ratio (the sum of your monthly debt payments, including your new mortgage, divided by your gross monthly income) to be less than a certain limit (on average, 40%). For example, if you earn $60,000 a year ($5,000 a month) and have a $300 student loan payment, a $300 car payment and are applying for a mortgage with a $1,000 payment, your ratio is 0.32 and OK.

Let’s say, however, you’re a recent law school grad with $1,400 in student loan payments, no other debt, earning $85,000 a year and applying for a mortgage with a $1,500 monthly payment. This puts your ratio at 0.41—too high to qualify for the mortgage.

Your options are to:

- Reduce the mortgage payment (by putting more money down, extending the term, or finding a cheaper house).

- Reduce your monthly student loan payments.

Unfortunately, paying extra towards your student loans does not reduce your monthly payment—it merely shortens the number of payments you’ll make. In this case you’ll need to talk to your student loan servicer about extending your term or refinancing.

There are lots of great options available if you want to go this route. Earnest is one of our favorite lenders right now – they provide some of the lowest refinancing rates available, and their application process is quick and easy.

Another route you have available to use services and search through a company like Credible, which scours the lending marketplace and presents you with the best terms available for your specific student loan needs, be it private student loans or refinancing. Credible also offers personal loans and other services.

Obviously, these options are not ideal because they’ll cost you more money in interest in the long-run. But, if your goals include repaying your student loans in 10 years but also buying a home now, you can extend the term of your loan repayment, buy the house, and then resume making extra monthly payments towards your loans so they’re paid off according to the regular schedule.

Finally, enjoy some money now

One final, if a controversial piece of advice: One good reason not to get overzealous repaying student loans early is to enjoy some money now. Most of us will have more money as we get older thanks to rising salaries and savings we build up over time. Of course, you won’t be young forever. One of life’s cruel jokes is that when you’re young and active you have no money and when you’re old you have money but less vitality.

Don’t go screw up your future finances to do it, but don’t bank so much on retirement that you neglect to travel, dine, and experience new things now.

Summary

As a recap, the upside to paying off student loans early are:

- A guaranteed return on your money by avoiding future interest

- Getting out of debt faster

The upsides of investing are:

- Potential for a greater long-term return

- Can cash out if absolutely necessary*

*Don’t underestimate this; having access to your wealth is important. When you repay debt, you increase your net worth but reduce your liquid wealth. Having $10,000 less student loan debt is not the same as having $10,000 in a mutual fund.