Higher mortgage rates means that a bigger percentage of your monthly mortgage payment will go toward interest, not the loan principal. That, in turn, affects how much you will be pre-approved to borrow.

Higher mortgage rates means that a bigger percentage of your monthly mortgage payment will go toward interest, not the loan principal. That, in turn, affects how much you will be pre-approved to borrow.

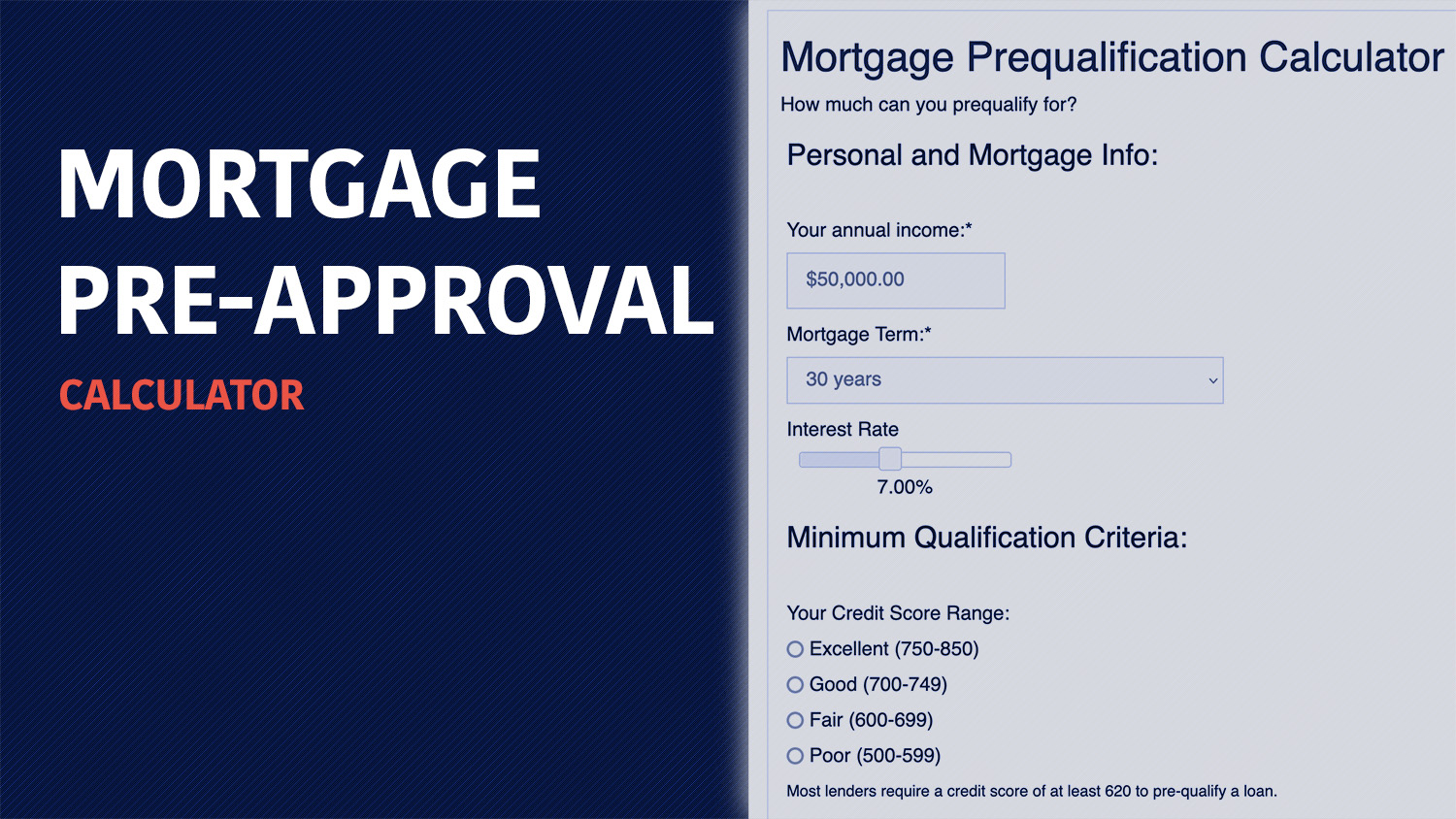

This mortgage pre-approval calculator will help you better understand how much house you can afford and what mortgage amount you’re likely to be qualified for.

MRC is the Internet's leading source for mortgage rates from dozens of lenders.

Answer a few basic questions to see your rates.

- Purchase or refi

- Won't affect your credit

- Options for first-time buyers, VA and FHA loans

- Must provide your email address

How to use the mortgage pre-approval calculator

This mortgage pre-approval calculator shows you how much home financing you can qualify for. Here’s how to fill out each of the fields to get your own prequalification estimate:

Personal and mortgage information

- Annual income — Enter your gross income, which is your total income before taxes and other payroll deductions, like your health insurance and retirement plan contributions. Lenders base your income on your gross income, not your net (after-tax) income.

- Mortgage term — This can be anywhere from 10 to 30 years, but entering 30 years will have the lowest payments, and enable you to qualify for the highest loan amount.

- Interest rate — This is the rate you expect to pay on the loan you’ll receive. Based on current rates, 7% is a safe estimate. But be aware that based on your credit situation, you may not qualify for the lowest rate available.

Minimum qualification criteria

- Your credit score range — If you don’t know your score, you can sign up for a free credit score service. Just keep in mind your free credit score may be different from what a mortgage lender will pull. If your credit score is below 620, you’ll likely have difficulty getting a mortgage.

- Have you been employed full-time for the past two years? — Mortgage lenders generally require a minimum full-time work history of at least two years. However, there are exceptions if you are a recent college graduate or recently discharged from the military.

- Are you saving toward a down payment? — Though mortgage lenders prefer borrowers to make a minimum down payment of 20% of the purchase price, they’ll go as low as 3%. The one exception is a VA mortgage, which provides 100% financing and requires no down payment.

- Have you been foreclosed on in the past seven years or filed for bankruptcy in the past four years? — The bankruptcy and foreclosure rules to qualify for a mortgage are a bit complicated. On bankruptcy, you’ll be eligible after four years. However, you can qualify in as little as two years if the reason for the bankruptcy was due to extenuating circumstances, like a major medical event or extended job loss. On foreclosures, the waiting period is seven years, but it can be reduced to three years with extenuating circumstances.

Monthly recurring payments

- Your total recurring monthly debts — These include loan payments, such as student loans, car loans, and credit cards, as well as alimony or child support payments if you’re required to pay either. However, you don’t need to include recurring expenses like utilities, insurance premiums, or contributions to retirement plans.

- Monthly property tax cost — We’ve gone with $195 as the national average; however, it’s better if you can get the actual figure for your area. Real estate taxes can vary considerably from one state to another, or even from one municipality to another.

- Monthly home insurance cost — This is one of the most difficult figures to estimate because it varies by location, property value, and even property type. The calculator includes $140 per month, since it’s the national average.

Once all fields have been entered, hit the Check button. You’ll be provided both the recommended maximum mortgage loan amount and the monthly mortgage payment.

Be aware that the monthly mortgage payment is just the principal and interest you’ll be paying on your loan. It won’t include the monthly property taxes or monthly home insurance premiums. You’ll need to add these expenses to the mortgage payment to determine what your total house payment will be.

Mortgage prequalification vs. pre-approval

There’s an important difference between a mortgage prequalification and a mortgage pre-approval.

Prequalification

When you apply for a mortgage prequalification, the lender is letting you know how much mortgage financing you qualify for based on the information you supply. That is, the lender may take your information online or over the phone, without verifying it with supporting documentation.

A mortgage prequalification, therefore, represents an opinion based on the information you supply, subject to verification of everything.

Pre-approval

A mortgage pre-approval happens when you submit an application — complete with supporting documentation — that’s been underwritten by the lender and approved. Under ideal circumstances, you’re fully approved based on your income, credit, and assets. The only thing you’ll need is an accepted contract offer on a home and an appraisal.

A mortgage pre-approval is what a real estate agent or property seller will be looking for you to supply. Because it will indicate you are a pre-approved borrower, it carries substantial weight when you make an offer on a home.

View our mortgage pre-approval checklist to see what info and documentation you’ll need to supply.

Summary

This mortgage prequalification calculator gives you an estimate of how much you can borrow, which will help you narrow down your home search to properties that fit within your budget.

Just remember that a mortgage prequalification is based on the information you supply and isn’t a guarantee that you’ll actually get approved for a mortgage. A mortgage pre-approval, on the other hand, is a more thorough process that involves submitting supporting documents and having your application underwritten by the lender.

MRC is the Internet's leading source for mortgage rates from dozens of lenders.

Answer a few basic questions to see your rates.

- Purchase or refi

- Won't affect your credit

- Options for first-time buyers, VA and FHA loans

- Must provide your email address